- 180+ Forex brokers reviewed using the latest data.

- Helpful broker lists so you can compare them side-by-side.

- Detailed and independently written expert reviews.

- In-depth educational resources for beginner traders.

-

Best Forex Brokers

Our top-rated Forex brokers

-

Brokers for Beginners

Start trading here

-

Forex Demo Accounts

Learn to trade with no risk

-

ZAR Trading Accounts

Save on conversion fees

-

Lowest Spread Brokers

Raw spreads & low commissions

-

ECN Brokers

Trade with Direct Market Access

-

No-deposit Bonuses

Live trading with no deposit

-

High Leverage Brokers

Extend your buying power

-

Islamic Account Brokers

Best accounts for Muslim traders

-

Market Maker Brokers

Fixed spreads & instant execution

-

All Trading Platforms

Find a platform that works for you

-

TradingView Brokers

The top TradingView brokers

-

MetaTrader4 Brokers

The top MT4 brokers in SA

-

MetaTrader5 Brokers

The top MT5 brokers in SA

-

cTrader Brokers

The top cTrader brokers in SA

-

Forex Trading Apps

Trade on the go from your phone

-

Copy Trading Brokers

Copy professional traders

Forex Broker Ratings

Discover our top ranked brokers!

FXScouts Podcast: Let’s Talk Forex

Season 3 just dropped! We cover how to minimise risk in Forex trading, trading psychology, Forex terminology, trading strategies, and interviews with top brokers.

Events & Webinars

Your one-stop shop for free educational events and webinars for traders of all experience levels from the best brokers in the world. These events cover all aspects of trading, including trading basics, fundamental analysis, technical analysis and more.

Discovering Reliable and Regulated Forex Brokers: Your Ultimate Guide

Access our comprehensive, up-to-date list of the best Forex brokers in South Africa, complete with in-depth reviews and ratings. We grade each broker using over 200 metrics and strictly evaluate them based on their regulation, fees, platform options, education, and customer support.

Our evaluation is combined with input from real traders, in order to give you a well-rounded picture of each broker’s strengths and weaknesses. Use our site to find the South African broker that suits your trading goals, experience level, and budget, and find out more about their latest promotions and bonuses.

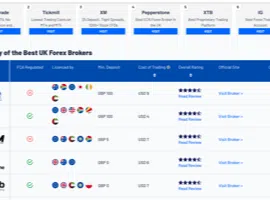

Our Top Rated Forex Brokers 2024

RegulatorsASIC, CMA, CySEC

- Leverage500:1

- PlatformsMT4, MT5, cTrader

- Min. Spread0.0

- Broker TypeECN/DMA

- Min. DepositAUD 100

RegulatorsASIC, CBI, CySEC

- Leverage400:1

- PlatformsMT4, MT5, Avatrade Social

- Min. Spread0.9

- Broker TypeMarket Maker

- Min. DepositZAR 1900

RegulatorsASIC, BaFin, CMA

- Leverage400:1

- PlatformsMT4, MT5, cTrader

- Min. Spread0.0

- Broker TypeNDD

- Min. DepositUSD 0

Unlock the Secrets to Successful Forex Trading in South Africa

Forex trading is accessible to everyone and offers the potential for significant returns, but it is important to approach it cautiously to avoid losing money. Forex traders in South Africa should choose a reputable and regulated broker to avoid getting scammed, educate themselves on Forex trading, create a trading plan and stick to it, develop a risk management strategy, practice trading on a demo account, stay informed and educated, and follow the global financial market news.

Latest Forex News and Analysis

Keep up to date with the latest market news and analysis. Our research team keeps a close eye on developments in the financial markets and Forex industry.

FXScouts Podcast: Let's Talk Forex

Season 3 just dropped! We cover how to minimise risk in Forex trading, trading psychology, Forex terminology, trading strategies, and interviews with top brokers.

Best Forex Brokers for Beginners

Explore top forex brokers tailored for beginners, ensuring a smooth start in the trading world.

Compare Forex Brokers Side-by-Side Using Complete and Accurate Data.

We are big believers in transparency. To help you make an informed choice, we publish our comprehensive broker comparison process and constantly update our State of the Forex Market report.

FP MarketsPepperstone

RegulatorsASIC, CySECFCA, ASIC

Leverage500:1400:1

PlatformsMT4, MT5MT4, MT5

Min. Spread0.0 pips0.0 pips

Min. DepositAUD 100USD 0

AvaTradePepperstone

RegulatorsFSCA, ASICFCA, ASIC

Leverage400:1400:1

PlatformsMT4, MT5MT4, MT5

Min. Spread0.9 pips0.0 pips

Min. DepositZAR 1900USD 0

PepperstoneIC Markets

RegulatorsFCA, ASICCySEC, ASIC

Leverage400:1500:1

PlatformsMT4, MT5MT4, MT5

Min. Spread0.0 pips0.1 pips

Min. DepositUSD 0USD 200

What is Forex Trading?

Forex trading, derived from Foreign Exchange, is the process of exchanging one currency for another through secure online platforms connected to Forex brokers. Forex trading is a popular way for South Africans to profit from trading the world’s largest financial market, with a daily trading volume of over $5.3 trillion. Forex trading in South Africa is legal and regulated, and South African Forex traders are protected by the Financial Sector Conduct Authority (FSCA).

Every day, thousands of South African traders buy and sell currency pairs, such as the ZAR/USD, hoping to make a profit through the fluctuations in exchange rates. It´s difficult to predict the changes in exchange rates between currencies. They are determined by complex economic, political, and technical factors, making Forex trading both a risky yet potentially profitable career.

Access all our Forex Guides

When it comes to navigating the world of Forex trading, our team conducts extensive research to bring you the most reliable, unbiased broker reviews. We also provide insightful guides that tackle all kinds of questions to help you make the right choice based on your trading needs. Access all our broker reviews, top lists, and guides here.

Major Currency Pairs

EUR/USD

Find the top brokers for trading the EUR/USD currency pair. Get access to live charts, up-to-date news and market analysis.

GBP/USD

Discover the best brokers for trading GBP/USD. Stay informed with live charts, current news and market analysis.

USD/CHF

Trade the USD/CHF currency pair using the top brokers. Access market trends, real-time charts and expert analysis.

USD/JPY

Trade the USD/JPY currency pair with top brokers. Stay informed with live charts, news, and market analysis.

About us

We’re a global team of Forex professionals. Our mission is to decrease the number of people who get scammed or lose money in Forex trading by providing education, highlighting serious brokers, and assisting Forex traders in finding the best-regulated broker for their needs. We test and review Forex brokers and create high-quality and meaningful educational content that furthers our readers’ interest in trading and education.

To read more about our methodology and how we rate Forex brokers, read all about our review process here. When you sign up for an account through our links, we sometimes earn a commission, which enables us to continue making our website better for you. To read more about who we are, how to contact us, and how we work, read our about us page.

FxScouts is wholly owned and operated by FxScouts Group AB, a privately held company founded in 2012. FxScouts Group AB is registered in Nyköping, Sweden and owns and manages all the brands and domains in the FxScouts network.

Stay updated

This form has double opt in enabled. You will need to confirm your email address before being added to the list.